Abstract In 2017, the photovoltaic industry chain will go from the upstream polysilicon to the downstream components, and will enter the era of overcapacity. Some PV companies have a worrisome outlook. The house leaks to the night rain: On April 27th, the US solar company Suniva drew the US International Trade Commission to ask for...

In 2017, the photovoltaic industry chain will go from the upstream polysilicon to the downstream components, and will enter the era of overcapacity. Some PV companies have a worrisome outlook. The house leaks to the night rain: On April 27th, the US solar company Suniva asked the US International Trade Commission to apply "201 clause" to implement trade remedy for all solar photovoltaic products not made in the United States, setting a minimum import price; May 10 On the same day, the General Department of the National Energy Administration issued a document on the scale of strict photovoltaic power plants. According to the documentation requirements, in addition to distributed photovoltaic power plants in the next three years, there will be no market for large power plants.

1. How serious is the overcapacity in the PV industry chain?

1. Polysilicon production capacity

According to the Silicon Industry Branch, by the end of 2017, China's polysilicon production capacity will reach 285,000 tons, which can meet the domestic production of 61 GW of solar cells. The self-sufficiency rate of China's photovoltaic polysilicon raw materials exceeds 100%.

At the end of 2016, China's polysilicon production capacity is 210,000 tons, which can meet the demand for all raw materials for domestic 45 GW battery production. However, polysilicon is still expanding its production capacity in the country. In 2016, Dongfang hopes to announce the construction of a 120,000-ton polysilicon project in Xinjiang, with an expected cost of 40 yuan per kilogram and supporting 8GW of single crystal projects. In 2017, GCL-Poly announced the joint construction of 60,000 tons of polysilicon with a number of PV giants in Xinjiang. It is estimated that the capacity at the end of 2018 will exceed 100,000 tons. The production capacity of other major polysilicon enterprises in 2016 is: 26,000 tons in Xinjiang, 16,000 tons in Luoyang, 12,000 tons in Daquan, 13,000 tons in Asian silicon, 17,000 tons in Sichuan Yongxiang and 10,000 tons in LDK. The output of these seven polysilicon enterprises accounts for about 80% of the national production.

2. Silicon wafer production capacity

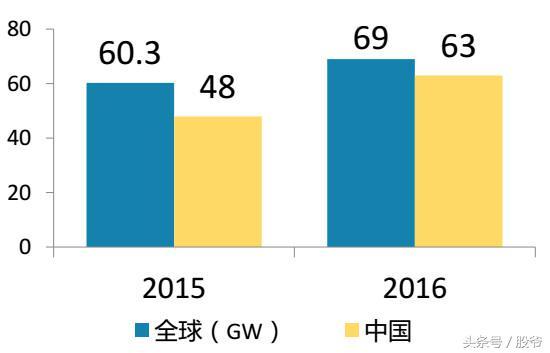

From Figure 2 we can see that in 2016, the global silicon wafer production capacity was 69GW, the foreign production capacity was 6GW, and the domestic production capacity was 63GW. If 2017 global PV market still maintains the same scale growth of 7Gw, and the growth market share is entirely occupied by domestic wafer manufacturers, in addition, the foreign silicon wafer production capacity of 6GW is half, and the domestic market share of silicon wafer manufacturers is just 10GW. In 2017, the newly added wafer production capacity is as follows: Longji added 4.5GW single crystal, Central added 5GW single crystal, Jinglong Group added new single crystal production capacity 1.5GW, GCL new single crystal production capacity 2Gw, Ningxia Zhongwei Yinyang Adding 1Gw of single crystal production capacity, 1.4GW of new single crystal production capacity of Suzhou Jingying Optoelectronics, 1GW of new single crystal production capacity of Jingke, and the remaining new single crystal production capacity of 2GW, the number of new single crystals will be calculated in 2017. The production capacity is 18.4GW. The newly added capacity of polycrystalline diamond wire cutting is 9.45GW (the number of diamond-cutting polycrystalline wafers increased by 20%, resulting in new polysilicon production capacity of 9.45GW), so there will be 17.85GW of silicon wafer overcapacity in 2017. A part of the polysilicon wafers with too high production costs will undoubtedly be eliminated.

Second, the house leaks and even the night rain

On April 27, 2017, US solar company Suniva asked the US International Trade Commission to apply “Article 201†to implement trade remedy for all solar photovoltaic products not manufactured in the United States and set a minimum import price. Compared with the "double-reverse" clause, the US "Article 201" is more arbitrary and more lethal. If Suniva's application is approved, the global PV trade war will be fully upgraded, and the PV market will usher in an uncompromising catastrophe!

Subsequently, on May 10, 2017, the General Affairs Department of the National Energy Administration issued the Notice on the Annual Construction Scale Plan for the Revenue of the 13th Five-Year Plan for Renewable Energy, requesting the provinces to submit renewable energy from 2017 to 2020. The annual construction scale will be strictly implemented according to the plan after it is determined, and it cannot exceed the scale! Among them, photovoltaic requirements:

1) The total scale shall be implemented in accordance with the grid-connected scale target proposed in the “13th Five-Year Plan for Solar Energy Developmentâ€, namely 105GW.

2) Distributed photovoltaic power generation, decentralized wind power and biogas power generation are not subject to annual new construction scale restrictions in various regions.

According to the statistics of the National Energy Administration on May 4, as of the first quarter of 2017, 84.63GW has been connected to the grid. This year, there are 5.5GW front-runners, 5.16GW photovoltaic poverty alleviation, and 8GW ground power stations have not been completed. Over 100GW at the end of 2017. There is no suspense. In other words, in addition to distributed photovoltaic power generation in the next three years, large-scale photovoltaic power plants have no indicators, so the photovoltaic market will be worried in the next three years! ! Although distributed PV is not limited, after all, the amount of distributed PV is too small, how to support such a huge photovoltaic capacity in China?

Third, photovoltaics fully open the shuffling mode, how many PV companies can survive in the storm?

On the same day that the National Energy Administration issued a notice, Solarworld AG declared bankruptcy and the flagship of Germany's last solar energy company sank. The bankruptcy of Solarworld AG announces that PV companies are fully open to shuffling! This round of shuffling will be more cruel than the previous round. Photovoltaic companies in Japan and the United States will be baptized, and companies that do not have competitive advantages in Chinese PV companies will not be spared.

Basin Faucet

A Basin Faucet (also spigot or tap: see usage variations) is a valve controlling the release of a liquid that enabling washing and drying in the bathroom.

Basin Faucet,Minimalist Basin Faucet,Basin Faucet For Bathroom,Wall Mounted Mixer Basin Faucets

Kaiping Jenor Sanitary Ware Co., Ltd , https://www.sanitaryjenor.com